“Go West” and China’s Inland Gateway Cities

This year marks the 20th anniversary of China’s “Go West” state-level strategy.

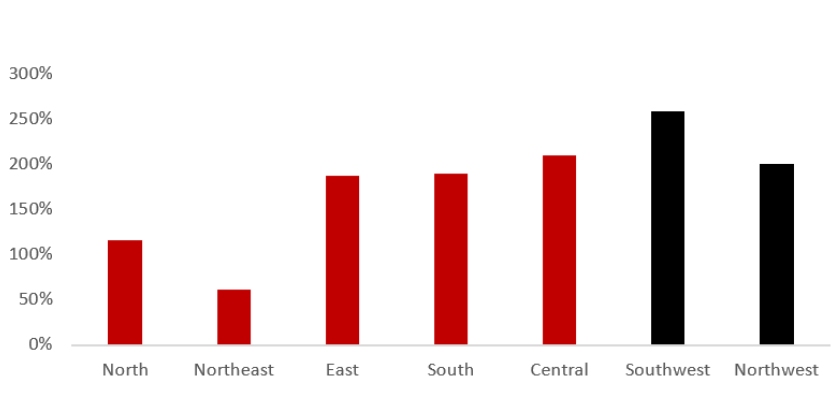

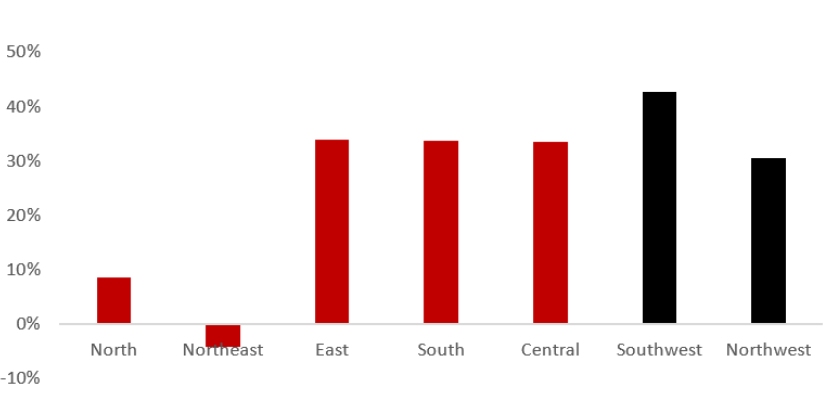

Twenty years ago, less than 50% of China’s population lived in urban area (as compared with 60% in 2019), and differences between the East (coastal) and the West (inland) was huge. Since then, infrastructure and real estate construction fuelled the pace of urbanisation, whilst inland gateway cities such as Chengdu, Chongqing and Xi’an, gained unprecedented momentum with an influx of capital and labour forces. During 2009-2019, Southwest China’s GDP recorded cumulative growth of 259%, outpacing all other regions in China. Growth was particularly strong during the period between 2016 and 2019.

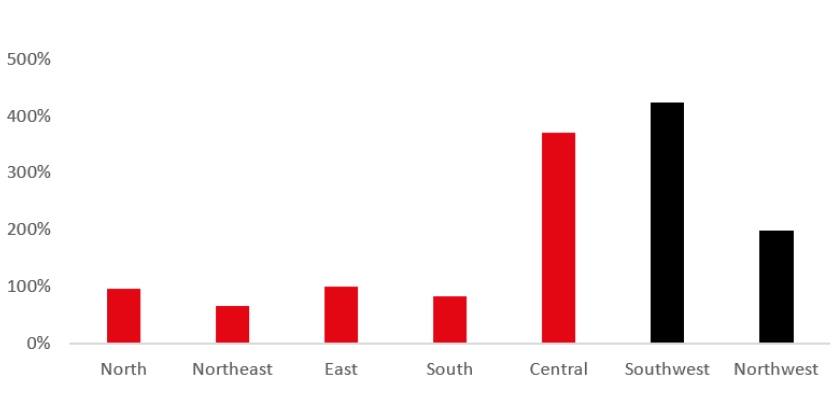

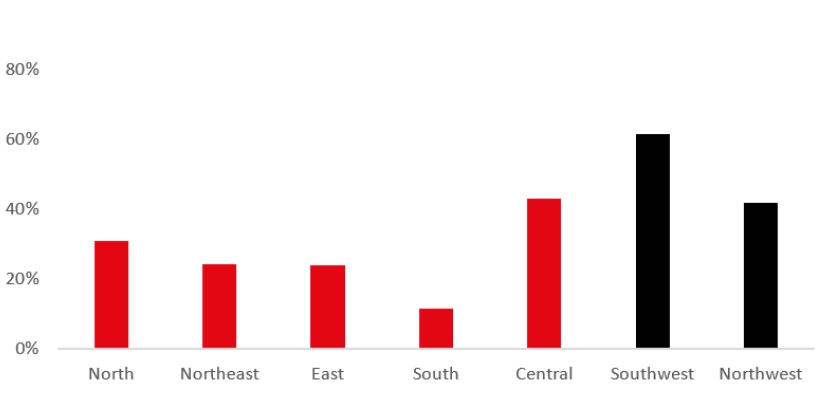

Figure 1: The Growth of GDP and Cross-border Trade

GDP Growth (Nominal Rate)

2006-2019

2016-2019

Cross-border Trade Growth

2006-2019

2016-2019

Source: National Statistics Bureau of China

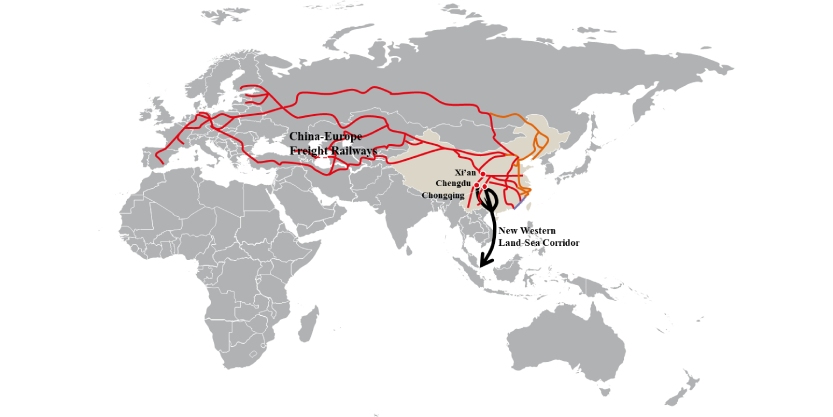

How did cities in West China, bearing stereotypical images of being under-developed, poor or even isolated throughout history, manage to catch up with coastal cities? The momentum started with the “Go West” strategy and has been enhanced by the Belt and Road Initiative, which aim to rebuild political and economic ties between China and the rest of the Eurasian Continent. China’s longest railway transported goods between the European, Middle East, and Central Asian countries and China. China’s inland areas, being far from the coast but adjacent to Central Asia, undoubtedly became a new frontier to these trading partners. That’s why cross-border trade achieved the highest growth in West China regions during the past few years.

Figure 2: The Belt and Road Initiative

Source: Adapted from Belt and Road Portal

In mid-May, the State Council released a new guideline of the “Go West” strategy. Establishing a modern industrial system, encouraging innovation, the integration of urban and rural areas and new infrastructure investment are key to this stimulus policy. Looking ahead, we expect a concentration of resources in high-profile city clusters, the forefronts being Jing-Jin-Ji (Beijing-Tianjin-Hebei), Yangtze River Delta and Guangdong-Hong Kong-Macau Greater Bay Area. The Chengdu-Chongqing city cluster should be the fourth economic powerhouse and also the first one in inland China.

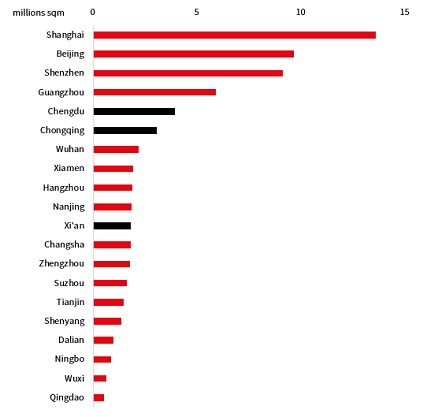

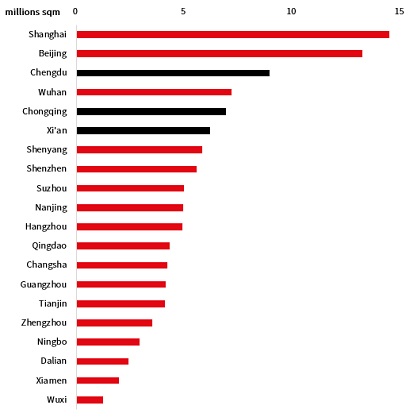

Over the past decade, West China cities have attracted trillions of dollars of capital inflow, accelerating commercial property development. As of end 1Q20, Chengdu and Chongqing have developed the largest Grade A office markets among non-tier 1 cities. In the retail sector, the development scale and intensity are even higher in Chengdu that surpasses Guangzhou and Shenzhen, whilst Chongqing and Xi’an rank fifth and sixth, respectively, in terms of prime retail stock.

Figure 3: Grade A Office and Prime Retail Stock

Grade A Office Stock

Prime Retail Stock

Source: JLL Research, 1Q20

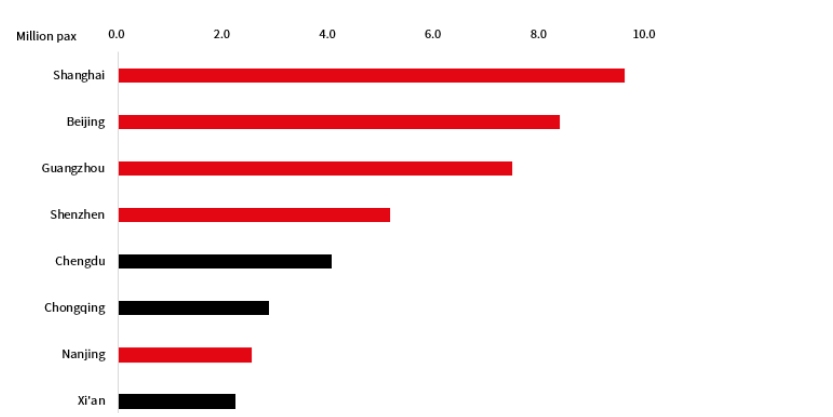

COVID-19 is causing the slowdown of economies and commercial activities worldwide. Nonetheless, West China cities have recovered rapidly from the pandemic. In April, Chengdu Airport reported the highest number of passengers countrywide, making the city reach an unprecedented rank among non-tier 1 cities. Metro data reassures our perception. It serves more than a signal of a city’s recovery, also confirming our viewpoint that West China represents the future.

Figure 4: 2020 Metro Foot Traffic Post COVID-19

Note: the city level daily highest foot traffic post to the COVID-19 outbreak

Source: China City’s Rail Transit Official Website

As China’s “Go West” strategy entered its third decade, we remain confident of the continued rise of West China and new opportunities for real estate investment in the hub cities of Chengdu, Chongqing and Xi’an.